San Diego, Calif., May 3, 2021 – Southern California Bancorp (the “Company”) (OTC Pink: BCAL), the holding company for Bank of Southern California, N.A. (the “Bank”) today reported financial results for the first quarter of 2021.

The comparability of financial information for the first quarter of 2021 to the first quarter of 2020 is affected by the Company’s acquisition of CalWest Bancorp (“CalWest”), effective May 29, 2020. Therefore, operating results for the first quarter of 2021 include the combined operations of both entities.

First Quarter 2021 Highlights

- Total loans increased to $1.4 billion, up $182.5 million or 14.8% from the previous quarter

- Total Paycheck Protection Program (PPP) originations of $229 million, with $118 million in forgiveness processed in the first quarter

- Total non-PPP loans increased to $903.6 million, up $76.2 million, or 9.2% from the previous quarter

- Net interest margin of 3.38%, excluding PPP loans the net interest margin was 3.64%

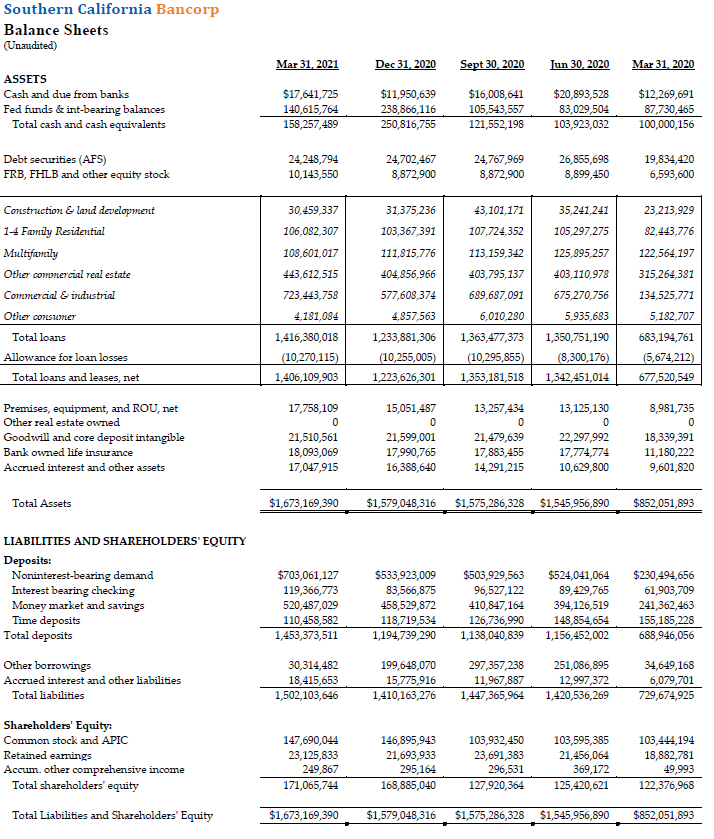

- Total assets increased to $1.7 billion, up $94 million or 6.0% from December 31, 2020

- Total deposits increased to $1.5 billion, up $258.6 million or 21.6% from the previous quarter

- Noninterest bearing demand deposits were 48.4% of total deposits

- Nonperforming assets to total assets of 0.05% at March 31, 2021

- Announced acquisition of Bank of Santa Clarita, which expands footprint into northern Los Angeles County and creates pro forma commercial bank with approximately $2.0 billion in assets

- Announced sale of three branches to align the Bank’s branch footprint to support its commercial banking strategy

- Continued status as well-capitalized, the highest regulatory capital category

“The first quarter of 2021 was a very strong quarter for the Bank’s loan originations, which included $76 million in net organic non-PPP loans and $229 million in PPP fundings,” said Nathan Rogge, President and Chief Executive Officer of Bank of Southern California. “Our non-PPP loan portfolio increased to $904 million, with the $76 million in loan growth fairly evenly divided between commercial and industrial loans, and commercial real estate loans. Our PPP loan portfolio increased to $513 million, up $106 million or 26% from the fourth quarter, as we processed $118 million in PPP loan forgiveness during the first quarter. Deposit growth was very strong, with total deposits increasing $259 million or 21.6%, including a $169 million increase in noninterest-bearing deposits, which were 48.4% of all deposits at the end of the first quarter. Credit quality remains very good with nonperforming assets to total assets of just 0.05% in the first quarter, down from 0.06% in the fourth quarter.”

“We made great strides in the first quarter toward the implementation of our commercial banking strategy,” said David Rainer, Executive Chairman of Southern California Bancorp and Bank of Southern California. “With the recently announced acquisition of Bank of Santa Clarita, we will be expanding our footprint into northern Los Angeles County with its attractive banking opportunities and partnered with a bank that has an established track record in the area and a customer service focus very similar to ours. This acquisition, combined with the sale of three branches that were not in alignment with our commercial banking strategy, moves us closer to the ideal branch network for our commercial platform, with a footprint that runs along the California coast from San Diego to Ventura County. Adding to that footprint, we opened branches in West Los Angeles and Encino during the first quarter and expect to open a branch in Westlake Village by July. We continue to add seasoned bankers and support staff to accommodate our expansion and the reception from the small to middle market businesses we target has been very positive.”

First Quarter Operating Results

Net Income

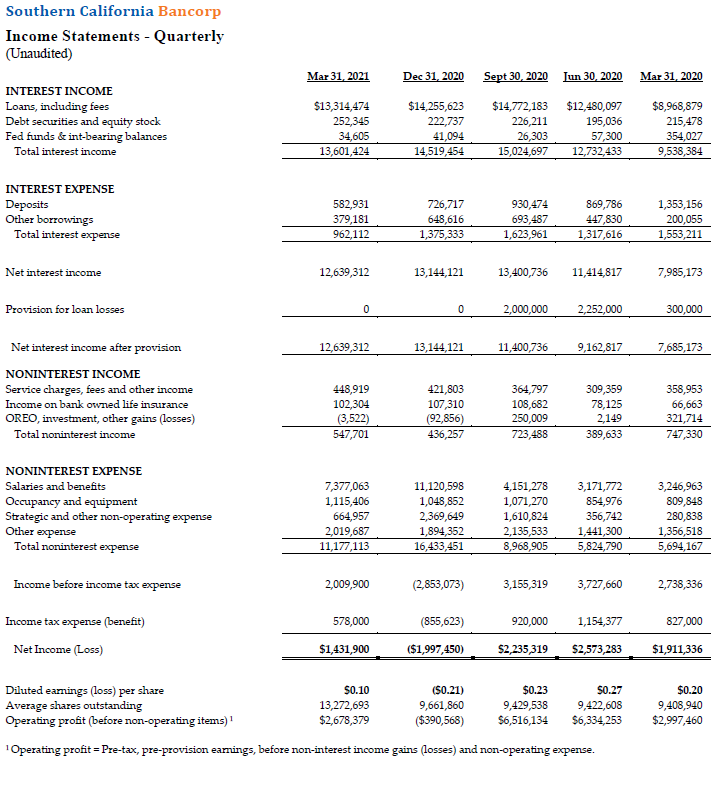

Net income for the first quarter of 2021 was $1.4 million or $0.10 per fully diluted share, compared with net income of $1.9 million or $0.20 per fully diluted share for the first quarter of 2020. The decrease in net income from the year-ago quarter was largely due to a $5.5 million increase in total expenses, primarily related to the acquisition of CalWest and the Company’s recent strategic expansion into Los Angeles County, partially offset by a $4.7 million increase in net interest income.

Net income for the first quarter of 2021 was $1.4 million or $0.10 per fully diluted share, compared with a net loss of $2.0 million or $(0.21) per fully diluted share in the fourth quarter of 2020. The increase in net income in the first quarter of 2021 was largely due to lower nonrecurring costs than recorded in the fourth quarter of 2020.

Net Interest Income and Net Interest Margin

Net interest income for the first quarter of 2021 was $12.6 million, an increase of $4.7 million or 58% from the first quarter of 2020. The increase was primarily due to an increase in average earning assets from the acquisition of CalWest, PPP originations and the Company’s expansion into Los Angeles County.

Net interest margin for the first quarter of 2021 was 3.38%, compared with 3.98% in the same quarter of the prior year. The decline in the net interest margin of the first quarter of 2021 was largely due to the decrease on loan yields and yield on average earning assets, to 4.08% and 3.63%, respectively, from 5.32% and 4.76%, respectively, in the prior year. The decline in loan yields was largely due to the 150 basis points reduction in interest rates in March 2020. Excluding PPP loans, the net interest margin would have been 3.64% in the first quarter of 2021 and 3.74% in the fourth quarter of 2020.

Net interest income for the first quarter of 2021 was $12.6 million, compared with $13.1 million for the fourth quarter of 2020. The decrease was primarily due to a lower effective yield on PPP loans and lower fair value fee accretion on loans acquired in the 2020 CalWest acquisition. Interest expense in the first quarter of 2021 was $962,000, a decrease of $413,000 or 30% from interest expense of $1.4 million in the fourth quarter of 2020. The decrease was primarily related to a reduction in average borrowings associated with a reduction in borrowings from the Federal Home Loan Bank (FHLB) and paying off the Federal Reserve Bank’s PPP Liquidity Facility (PPP LF).

Net interest margin for the first quarter of 2021 was 3.38%, compared to 3.47% in the fourth quarter of 2020. The decrease in net interest margin in the first quarter of 2021 was largely due to a reduction in the yield on average earning assets to 3.63%, from 3.83% in the prior quarter.

Average loan yields in the first quarter of 2021, excluding PPP loans, were 4.74%, a decrease of 38 basis points from 5.12% in the prior quarter, with the decrease primarily related to the higher fair value accretion on loans acquired in the CalWest acquisition in the fourth quarter of 2020. Average PPP loan yields decreased to 2.90% in the first quarter, compared to 3.09% in the prior quarter, partially due to the longer contractual maturity on PPP loans made in 2021.

Cost of funding for the first quarter of 2021 was 0.28%, down from 0.38% in the previous quarter. A detailed comparison of interest income, yields, costs, and net interest income is included in the table below:

| Q1 2021 | Q4 2020 | |||||

| Interest Income on: | ||||||

| Total Loans | 13,314,474 | 4.08% | $14,255,623 | 4.36% | ||

| Loans excl PPP | 9,954,156 | 4.74% | 10,482,994 | 5.12% | ||

| PPP Loans | 3,360,318 | 2.90% | 3,772,628 | 3.09% | ||

| Investments | 252,345 | 3.02% | 222,737 | 2.61% | ||

| Fed Funds & Int Earning | 34,605 | 0.09% | 41,094 | 0.09% | ||

| Total Interest Income | 13,601,424 | 3.63% | 14,519,454 | 3.83% | ||

| Int Exp on Deposits | 582,931 | 0.18% | 726,717 | 0.25% | ||

| Int Exp on Borrowings | 379,181 | 1.54% | 648,616 | 0.94% | ||

| Total Interest Expense | 962,112 | 0.28% | 1,375,333 | 0.38% | ||

| Net Interest Income | 12,639,312 | 3.38% | 13,144,121 | 3.47% | ||

Non-interest Income

Total non-interest income for the first quarter of 2021 was $548,000, compared to $747,000 in the first quarter of the prior year. The decrease in the first quarter of 2021 was largely related to a gain on sale of securities of $322,000 in the first quarter of 2020, for which there was no corresponding transaction in the first quarter of 2021.

Total non-interest income in the first quarter of 2021 increased by $111,000 or 25.5% over the fourth quarter of 2020, primarily due to a loss on fixed asset disposal of $93,000 recorded in the prior quarter.

Balance Sheet

Assets

Total assets at March 31, 2021, were $1.7 billion, an increase of $821 million or 96% from March 31, 2020, and $94 million or 6% from December 31, 2020. The increase in total assets from the year-ago period was primarily related to a $764 million increase in deposits and a $49 million increase in shareholder equity from the December 2020 capital raise.

Loans

Total loans were $1.4 billion at March 31, 2021, an increase of $182.5 million or 14.8% from December 31, 2020, and $733 million or 107% from March 31, 2020.

The Company’s non-PPP loan portfolio had net organic growth of $76.2 million, or 9.2%, related to new and existing relationships, and ended the quarter at $903.6 million.

Included in loan growth in the first quarter was a $39.7 million increase in commercial and industrial loans, a $37.2 million increase in real estate loans, and a $106 million increase in PPP loans.

Deposits

Total deposits at March 31, 2021, were $1.5 billion, an increase of $258.6 million from the end of the prior quarter and an increase of $764.4 million from the year-ago period. Noninterest-bearing deposits at March 31, 2021, were $703.1 million or 48.4% of total deposits, compared to $534.0 million or 45.0% of total deposits at December 31, 2020, and $230.5 million or 33.4% of total deposits at March 31, 2020.

Asset Quality

Total non-performing assets were $0.8 million or 0.05% of total assets at March 31, 2021, compared with $0.9 million or 0.06% of total assets at December 31, 2020.

The Company had $15,000 in net recoveries in the first quarter of 2021, compared with $11,000 in net recoveries in the first quarter of 2020 and $41,000 in net charge-offs in the fourth quarter of 2020.

The Company recorded no loan loss provision in the first quarter of 2021, after recording $4.6 million in provisions for the full year of 2020, and the allowance for loan and lease losses (ALLL) remained at $10.3 million at the end of the first quarter of 2021. The Company continues to monitor macroeconomic variables related to COVID-19 and believes it is adequately provisioned for the current environment. Management will continue to monitor and manage the loan portfolio to minimize potential future losses.

As the initial onset of economic uncertainty became clearer, many customers who elected a payment deferral have been returned to paying status; a total of $165 million in loans have reinstated their normal loan payments. Of the remaining eight loans currently on deferral, the following table details the exposure by industry:

| Industry | Outstanding Loan Amounts

($ in 000) |

Number of Loans |

| Hotels & Food | $1,677 | 1 |

| Real Estate, Rental & Leasing | 17,839 | 4 |

| Health Care | 1,192 | 2 |

| Other | 325 | 1 |

| Total | $21,033 | 8 |

Relevant reserve ratios compared to the prior quarter are as follows:

| Q1 2021 | Q4 2020 | Q1 2020 | |

| ALLL to Total Loans | 0.73% | 0.83% | 0.83% |

| ALLL and Loan Fair Value Credit Marks (LFVCM) to Total Loans | 1.00% | 1.18% | 1.07% |

| ALLL and LFVCM to Total Loans, excluding PPP Loans | 1.57% | 1.76% | 1.07% |

Liquidity and Capital

The Bank has ample liquidity resources to meet its customers’ needs, with the 21.6% growth in total deposits in the first quarter, as well as through both the FHLB and the PPP LF. At March 31, 2021, combined borrowing capacity available at both the FHLB and through PPP LF was over $760 million, with outstanding borrowings under these facilities of $10 million.

The significant growth in PPP loans over the past 12 months has been funded through a combination of increased DDA accounts, generally associated directly with the PPP Loans, borrowings under PPP LF, and other sources. At March 31, 2021, the Bank’s PPP loan portfolio was entirely funded by Bank deposits.

PPP loans are considered zero risk-weighted assets and PPP LF advances are not counted in the leverage ratio. As such, preferential capital treatment of PPP LF advances, as well as the private placement completed in December, have helped maintain the Bank’s leverage capital ratio and total risk-based capital ratio at 10.9% and 18.6%, respectively, for the quarter ended March 31, 2021.

FORWARD-LOOKING STATEMENTS

This news release may include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Exchange Act of 1934, as amended, and Southern California Bancorp (the “Company”) intends for such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. Future events are difficult to predict, and the expectations described above are necessarily subject to risk and uncertainty that may cause actual results to differ materially and adversely. Forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts. They often include the words “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” or words of similar meaning, or future or conditional verbs such as “will,” “would,” “should,” “could,” or “may.” These forward-looking statements are not guarantees of future performance, nor should they be relied upon as representing management’s views as of any subsequent date. Forward-looking statements involve significant risks and uncertainties and actual results may differ materially from those presented, either expressed or implied, in this news release. Factors that might cause such differences include, but are not limited to: the effects of the COVID-19 pandemic, or other similar outbreaks, including the effects of the steps being taken to address the pandemic and their impact on the Company’s markets, customers and employees; the ability of the Company to successfully integrate the business of Bank of Santa Clarita or if the integration becomes more difficult, time-consuming or costly than expected; expected revenue synergies and cost savings from the merger with Bank of Santa Clarita may not be fully realized or realized within the expected time frame; revenues following the merger may be lower than expected; customer and employee relationships and business operations may be disrupted by the merger; the ability to obtain required regulatory and shareholder approvals; the ability to complete the merger on the expected timeframe may be more difficult, time-consuming or costly than expected; the Company’s ability to successfully execute its business plans and achieve its objectives; changes in general economic and financial market conditions, either nationally or locally, in areas in which the Company conducts its operations; changes in interest rates; continuing consolidation in the financial services industry; new litigation or changes in existing litigation; increased competitive challenges and expanding product and pricing pressures among financial institutions; legislation or regulatory changes which adversely affect the Company’s operations or business; loss of key personnel; and changes in accounting policies or procedures as may be required by the Financial Accounting Standards Board or other regulatory agencies.

The Company undertakes no obligation to publicly revise these forward-looking statements to reflect subsequent events or circumstances.

Click sheet for larger image.